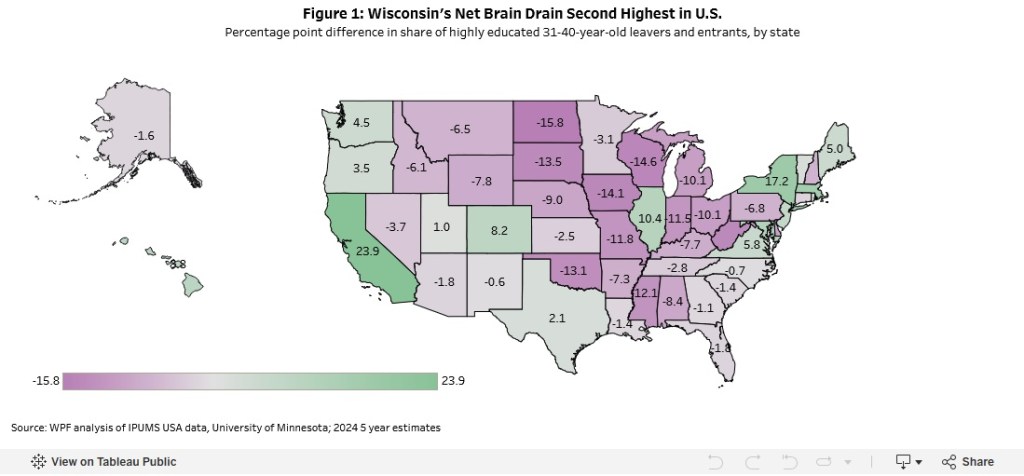

Wisconsin’s net brain drain ranks second nationally, behind only North Dakota (see Figure 1). This is a slight improvement from 2009, when Wisconsin’s net brain drain (-15.3 percentage points) was the highest in the nation. Most other Midwestern states have experienced similarly high rates of net brain drain, with the exception of Illinois, which stands out as the region’s only net “brain‑gain” state (+10.4 points). Nationally, a few other states with strong metropolitan hubs — such as Virginia (+5.8 points) in the Southeast and Colorado (+8.2) and Utah (+1.0) in the West — defy regional brain‑drain trends…

While brain drain measures the educational gap between movers and entrants, it does not account for the volume of people moving. A state may lose more highly educated residents than it gains, but the impact is far greater when large numbers of people are leaving, especially when the state has a less educated population to begin with.

This dimension is captured in Figure 4, which compares each state’s net brain drain rate against its cumulative domestic migration rate from 2020 to 2024 using data from the U.S. Census Bureau’s Population Estimates Program. Domestic net migration reflects only movement of U.S.-born adults — regardless of age — between states; it excludes births, deaths, and international migration. To help interpret these patterns based on a state’s educational foundation, Figure 4 also groups states by the educational level of their birth cohort—high, middle, and low terciles—based on our brain drain analysis.

Three quick thoughts:

It appears that the national map shows patterns: states with large and vibrant cities and metropolitan areas draw educated residents (think Boston, New York, Washington, D.C., Chicago, Houston, Dallas, Austin, Denver, Seattle, Portland, the Bay Area, and Los Angeles). It would be interesting to see this map by metro area rather than by state as there are likely differences within many states.

It would not be a big leap to go from this data analysis to an argument that cities and states should work even harder to attract young professionals or “the creative class.” How might this fit with efforts to serve and provide opportunities for current residents?

These figures reflect a dynamic context. Americans are less geographically mobile than earlier in the postwar era. Work from home opportunities are more plentiful for educated employees. Travel is relatively easy compared to the past. At the same time, cities and industries and cultural opportunities continue to cluster in particular places, attracting people and resources. How might this all affect brain gain and drain in the coming years?

The city of 33,000, a mixture of blue-collar workplace and lakefront playground, has benefited from several major developments in recent years. It is the home of a planned $300 million luxury hotel and townhouse development called SoLa (South of the Lake).

Last year, the addition of a second railroad track and new train station on the Metra South Shore Line cut commute times to Chicago to about an hour. It also is a gateway to the Indiana Dunes, which saw the number of visitors in recent years jump to around 3 million after it became a national park…

Other new developments include a $100 million, 12-story, mixed-use building at the train station called The Franklin, and 33 new single-family homes at Woodland Ridge…

But any plan to increase tourism in town will have to address a lurking eyesore that dominates the otherwise gorgeous lakefront: a giant concrete power plant cooling tower known to some locally as “the monstrosity,” that mars the views of the lakefront from every direction. Though the structure is for a coal power plant, visitors often assume it is for a nuclear plant.

NIPSCO, the company that operates the plant, says it plans to close the facility by the end of 2028. But NIPSCO also has plans to open a new gas-powered plant to power a coming data center, so it’s not clear what will become of the old plant.

The contrast is clear: waterfront property close to Chicago that is less desirable because of industry and a cooling tower. Move away from the industry and power plant and property values are higher and redevelopment opportunities more enticing. Removing a cooling tower several hundred feet tall would definitely change the local scenery. It may be a while – or never – before a residential tower reaches similar heights but the development already happening hints that more could be on the way.

This is certainly not the only waterfront community in the Midwest or in the United States with a power plant on the water. From places I have been in recent years, I also recall a power plant on the water in Sheboygan, Wisconsin. Or communities with major industrial works. Gary, Indiana is not too far away or the southeast side of Chicago.

With ongoing needs for power and resistance to power plants when they are proposed for certain places, where could a power plant like this go? Few people today would proposed a power plant along the water in or near population centers. Northern Indiana does have more open space away from the water – but land would need to be acquired, local approvals would be needed, demolition in Michigan City would have to happen. Power plants have to go somewhere, even if they are addressing issues raised by construction decisions from decades ago.

Some suburban street names are more unusual than others. I recently noted a neighborhood I occasionally drive past has religious street names. Here are several of them:

When many suburban subdivisions have bland names that invoke landscapes or desirable historical connections, why would this neighborhood invoke religious ideas?

I wonder how many suburban subdivisions have clearly religious street names. Given the number of religious congregations and groups in the United States, this might not be unexpected. However, I suspect this is quite unusual as developers want to appeal to a broad audience of possible homeowners and they want to connect certain ideas with the housing units.

(This would not often be a street name in newer subdivisions but would Church St/Ave/Rd/Ln be the most common “religious” street name in American suburbs?)

Reactions to the drones added at the Walmart Supercenter in Apopka have been mixed, with some residents like Brittany Nilsen saying she’d “absolutely” use the service for the sake of “convenience.”…

Some likened the noise to a police siren or fire truck but said they’d become accustomed to it.

In addition to the noise, other locals said they were worried about privacy and safety…

After arrival, the drone hovers about 20 feet above the drop zone and lowers the order down via the tether, with the drone itself never landing on a Walmart customer’s yard.

Imagine the air at roughly building height or tree top level with a steady stream of drones delivering packages from different suppliers. There would be noise. They would be part of the view when looking into the sky or looking into the distance.

But I was reminded this week of the ways that we now just accept delivery trucks all over the place. The trucks stop in roadways with their flashers on while the driver goes to the door to complete the delivery. They stop on narrow roads and busy roads. They add to traffic.

The benefit of both is that people get their desired objects without having to go to a store. The delivery comes directly to them. This modern convenience is expected and people will sacrifice for it to happen. Americans like driving and they are willing to put up with traffic and stopped vehicles to get their packages. Whatever downsides come with drones could be outweighed by packages coming via the sky.

Perhaps you have encountered this situation before: you are walking, biking, or driving through a neighborhood. Your nose suddenly picks up the smell of something grilling. Perhaps meat, maybe vegetables. It is tinged with smoke. It smells good. But where exactly is that smell coming from?

Much of our cooking or food preparation in the United States takes place inside. We have kitchens that facilitate storing and making food. Others can’t see it (unless there is a prominent window). They may occasionally smell it.

Even if people are grilling outside, it often takes place in backyards. Few Americans grill in their front yards or by their front doors. This is an activity typically reserved for the more private backyard.

So where is the grill smell coming from? One hint might be whether you can see smoke. Different grill techniques or different grilled items might lead to more smoke. Could you follow it to a source?

And even if you did identify the location of the good grilling smells, it would be rare in the American setting for a stranger to approach the grill and/or griller. Unless it is taking place in a more public setting (a front yard? a park? outside a restaurant?), the grilling is an activity for the griller and their acquaintances, not for a broader audience.

In the moment, you will have to settle for enjoying the grilling smells from a distance. Perhaps it will prompt you to grill yourselves or find someone who will grill for you. It is a good moment – but it is also a reminder of food preparation in private spaces.

Over the last few months, people have cut down surveillance cameras owned by the company Flock Safety with an electric saw in upstate New York, thrown paint on them in Oakland, California, and rammed a truck into them in Idaho. One man in Florida sits in a lawn chair holding up a piece of cardboard on a pole to block the camera’s view. City governments have joined in by deactivating the cameras or canceling contracts with Flock in Fort Collins, Colorado; Eugene, Oregon; Madison, Wisconsin; Knoxville, Tennessee; Syracuse, New York; and Walla Walla, Washington…

Flock says it has 120,000 automated license plate reader (ALPR) and pan, tilt, and zoom (PTZ) cameras deployed throughout the US, capturing tens of billions of data points a month. Flock’s ALPRs automatically scan every license plate that passes them, while the PTZs record live footage that can be reviewed and analyzed. Because Flock cameras are all connected, the result is a nationwide latticework of recorded activity. Across the majority of states, a police officer in one state can be alerted if a car they’re looking for pops up in another and can inform the local authorities…

Over the last few months, Flock has been making headlines for all the wrong reasons. Police have been caught using the system to stalk exes and colleagues, and journalists have reported that, contrary to the company’s claims that it only logs vehicles, the cameras can be used to track people.

As more Americans now respond to the cameras, which communities will end up cancelling contracts and which ones will keep them? The list above in the first paragraph involves smaller big cities. Does this mean opposition to cameras is primarily in such communities? Or would opposition to cameras drop (1) in places with higher crime rates or (2) in places with higher fear of crime?

It will also be interesting to see how local leaders in different kinds of communities respond to public pressure. Who will resist opposition and what reasons will they give? The company offers a defense of their product and its use; whether local leaders use similar lines remains to be seen.

This is Xanadu, the Computerized Home of Tomorrow, which opened its doors in 1983 in Florida, strategically located just a few miles from Disney World’s Epcot Center. Xanadu’s Yale-trained architect, Roy Mason, wanted to create a walk-through instruction manual for building a smart home. Mason saw this blurring of architecture and sociality as the answer to the many problems of the American family: loneliness, boredom, frustration, parent-child conflict, and general depression. The result proposed automation as remedy and liberation.

Much like the techno-pessimistic nightmare imagined by Ray Bradbury’s short story “The Veldt,” in which housekeeping and child-rearing are ceded to automated homes, Xanadu’s “electric hearth” was run by a “House Brain” to control life support functions. (The House Brain is, in a way, another term for mother.) Staffed by a robot dubbed Robutler that remediated paid servant labor, the house aimed to take over a wide variety of tasks — but only as the owners wished. The Brain, meanwhile, was a personal assistant, presaging the integration of Alexa and Siri into smart home systems. It was designed to provide customizability in managing various aspects of middle-class life. It could call local plumbers and neighbors, offer telemedicine, menu planning, and even outfit selection via an automated clothes-retrieval closet.

Xanadu was not the first of its kind. In 1957, Disney unveiled the House of the Future in collaboration with MIT and Monsanto, which sought to showcase the engineering and design versatility of plastics. Visitors of Tomorrowland walked through the attraction and marveled at its features — microwave ovens, wall-mounted TVs, adjustable sinks, modular bedrooms — which would, of course, become commonplace in the decades to come. Likewise, Xanadu invited thousands of guests each day to see a possible home of tomorrow, augmented by technology that could be customized to conform to the changing needs and shapes of American families…

This mixed temporality is a classic trick of the model home: The space is staged to prompt viewers to imagine bringing these systems into their own lives now, while also presenting a new ideal of futuristic living…

People do not live the same way at different time points. This is true because of a variety of factors, including technological change that can introduce new opportunities or challenges and design of objects and places. Daily life changes.

But does new technology necessarily go along with new design? Put another way: could we have new technology while living in a world that still looks like the 1970s or the 2000s? Or could we have new designs for houses and domestic life but no significant changes in technology?

These houses constructed decades ago put design and technology together: they were a package deal. But I would guess our average home technology has changed more than the average home design. Still relatively few American houses are fully modernist inside and/or outside. New homes continue to remix older design features.

And I wonder how much those future visions of American homes contended with the many homes built decades ago they will not be retrofitted or redesigned or redeveloped. Moving to futuristic design is a long process with the many housing units from previous eras still standing and serving their occupants well. Similarly, integrating technology in an older home might be a challenge. It is one thing to put an Echo on the counter; it is another to put in full house air conditioning or run wires through multiple walls.

In this fabulous alternative history of the modern world, the academic and “party historian” Imogen Willetts looks at the last 500 years of civilisation through the sometimes blurry lenses of its after-dark scenes, with fascinating results. She begins by trying to capture what it feels like to go on a big night out, focusing on a phenomenon that, in 1912, the sociologist Émile Durkheim labelled “collective effervescence”. In one passage, she explains this by referencing dancing as part of ancient tribal hunting rituals, listening to Charli xcx’s 365, or singing along to Sweet Caroline with tens of thousands of other people in a stadium.

This is no dry academic study, then, and its mix of historical research, critical theory and conversational references to pop culture makes for a bright and compelling read. What Willetts calls the “seemingly superficial act of getting gussied up to drink, dance, have fun and meet people” is, of course, much more than that, and she scratches away at the layers with skill. Nightlife can contain, or enable, rebellion, community, innovation, art, love, sex and political revolution. From Japan to France, from Shanghai to Germany, via many detours to the United States, she examines historical movements as they might be seen from dusk till dawn.

Part of the appeal of collective effervescence is that individual people get caught up in a scene or moment or crowd. It is not just doing something fun or unique; it is collective activity that is something different compared to what an individual can experience alone. It is about taking part in something bigger.

Do we have good predictors of when nightlife crowds or activities can turn into society changing moments or movements? Nightlife occurs regularly in many places; what helps it turn into something consequential or when it spills out beyond the initial gathering or activity?

And since I study suburbs, I wonder about the lack of nightlife in many suburban communities. This is part of the appeal to many; suburbs are quieter places for people to live. On the other hand, cities are known for more nightlife options. How much does this contribute to what many perceive to be a lack of interest in social change in American suburbs?

There is a category of places that we know but we do not know. In the United States where driving is a daily part of life, people regularly pass through neighborhoods, communities, and places in which they rarely or never stop. It is just along the way. The driver is just driving through. What do we know about such places? A few thoughts, with the example of Gary, Indiana in mind as I have driven back and forth past Gary many times (and only stopped there a few times).

We are limited to what we can see from a moving vehicle. Yet, we can see some things while driving by, even at fast highway speeds. We tend to see what is along major roads, which can include road signs, billboards, big box stores, exits and intersections, some smaller commercial and residential properties. Some of the signs and properties try to get our attention, often to tell us about a brand, product, place, or attraction. This might tell us about the biggest things to see and do. Passing by Gary via highway, I can see a minor league baseball stadium, steel mills, and some bigger downtown buildings. I can see highway exits and the kinds of establishments that gather there. I see signs for an airport and a few other things to do.

We hear or tell stories about these places. I have read about Gary, heard about Gary, talked about Gary. Some themes: created out of sand dunes as an industrial suburb, steel mills, the home of the Jacksons, decline and white flight, limited development and reinvestment, and new ideas for revitalization. As I drive by, how does what I see contribute to or refute those stories? How much am I fitting what I see to a narrative I already have?

The few stops I have made are different than just driving by. Setting foot in a community, driving at slower speeds and maybe walking around, provides a different experience. So does talking to people or taking a tour. It helps to slow down, get to a pedestrian level, and have time to observe and interact. (See earlier posts about how to know a suburb or community – first steps, deeper steps.)

I could come up with a list of many other communities where the same is true: I have driven through it or passed by it and know relatively little about it. And if we tend to emphasize getting to our destination rather than seeing what is on the way on the journey, we could go through or by places hundreds or thousands of times. Highways do not facilitate getting to know places; this seems to be part of the argument about what happens to Radiator Springs in the Pixar film Cars. Trains may offer different views (and maybe some more stops) at similar speeds while airplanes allow people to just hop even faster over places without even seeing them.

There are ways this could be addressed. Could we get more information about places as we pass them? This is hard to do on road signs. How about voice explanations in maps or GPS systems? How about using the voices of local residents to describe their community and tell stories of what has happened?

Despite Cook County residents’ long, loud complaints about out-of-control property taxes and government spending, a majority of them couldn’t be bothered to turn out to vote in recent elections when given the chance to decide whether taxes should be hiked.

About 1 in 5 eligible voters decided the outcome of costly binding property tax questions in various suburbs in the past couple of years, according to a new study from the Cook County treasurer’s office…

Voter turnout in primaries is typically lower than general elections as it is, and even fewer voters participate in local consolidated elections.

But the report also found participation dipped on ballots for property tax questions in particular. It floated a few reasons why people who do vote might skip referendums: the questions are often at the bottom of the ballot or confusingly written…

Previous reports from her office have highlighted higher turnouts in wealthier and whiter areas. While the income trends continued in the 2025 and 2026 elections, there was not enough data to see whether the racial trends shifted because most of the referendums were in majority white communities.

It sounds like the factors cited above could be addressed. Don’t bury them at the bottom of the ballot. Make sure they are written in clear language. Help people know what is on the ballot far ahead of time. Put the tax questions on the bigger election cycles. For those who want to promote good governance (rather than even the appearance of sneaking things through on the ballot), this is doable.

I wonder if there would be any traction for elected officials to run on the platform of getting more people involved in local political decisions. Rather than targeting a small portion of voters or a political base, could someone aim to get more people to decide questions like these about property taxes?